A tractor changes the economics of a farm, but it costs far more than a single season’s income. So the real question for most farmers in Northern Uganda is not whether to mechanize, but how to pay for it. The good news is that there are several genuine financing routes, and most of them are built precisely for people who don’t hold a bank-grade land title. This guide compares them honestly, with indicative rates and how to qualify.

- Few smallholders buy a tractor alone: most access one through a cooperative that pools savings and machines.

- SACCO loans lend against your savings and guarantors: no land title needed.

- The Microfinance Support Centre lends to cooperatives at roughly 8–9% a year, with asset-financing and leasing options.

- Match the loan to one harvest: over-borrowing against seasonal income is the most common trap.

Why banks rarely finance smallholders

Agriculture is the backbone of Uganda’s economy, yet it receives a small share of bank credit, and only a minority of farmers access formal loans at all. The reasons are structural: farmers work small plots, often without registered land titles to pledge as collateral; farm income arrives in lumps at harvest while bank loans demand fixed monthly repayments; and banks struggle to price the weather risk. Commercial-bank lending rates have averaged around 18–21% per year, with agriculture at the higher end.

That mismatch is why the most useful financing routes for a smallholder are the ones built around savings, groups and the harvest cycle, not a bank branch.

The financing routes, compared

| Route | Indicative cost | Best for | Collateral |

|---|---|---|---|

| SACCO / cooperative loan | ~2–3% per month | Members financing their share, inputs, working capital | Savings + member guarantors |

| Microfinance Support Centre (MSC) | ~8–9% per year | Cooperatives & groups buying shared equipment | Group accountability; asset itself |

| Uganda Development Bank (UDB) | ~10–12% per year | Larger projects, usually via a cooperative | Land, equipment, project cash flow |

| Asset financing / hire-purchase | Varies by supplier | Acquiring a specific machine over time | The asset itself (≈20% deposit) |

| Parish Development Model (PDM) | ~1% (revolving fund) | Subsistence households entering the money economy | Enterprise group membership |

| Commercial bank | ~18–21% per year | Established commercial farms with title | Land title, strong documentation |

Read rates carefullyA "2% per month" SACCO rate and a "12% per year" bank rate are not directly comparable until you check two things: per month vs per year, and flat vs reducing balance. Always ask a lender to express the total cost in shillings over the full term before you sign.

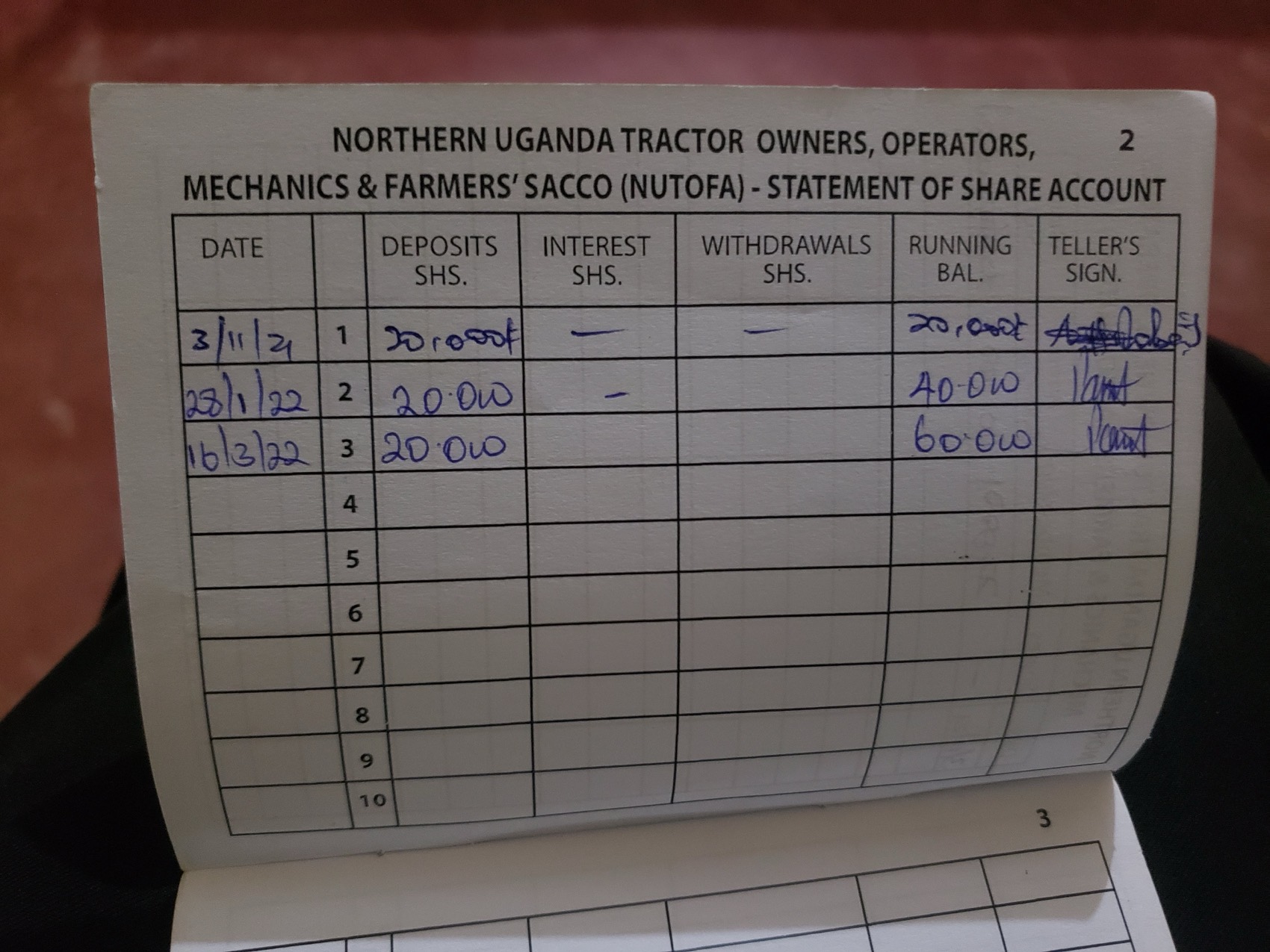

Route 1: Your SACCO

For most members, the first and best route is their own cooperative. A SACCO lends against your savings history and member guarantors, not a land title, so it reaches farmers banks won’t. Loan ceilings are typically a multiple of your savings (NUTOFA uses a three-times-savings rule), and repayment can be timed to your harvest.

A SACCO loan rarely buys a whole tractor outright, but it is ideal for financing your share of a group machine, implements, spares, fuel, or the working capital a season needs. And because the cooperative also runs the mechanization hub, the loan and the machine sit in the same place.

Route 2: The Microfinance Support Centre (MSC)

The MSC is a government-owned company set up to deliver affordable credit to the “active poor,” with a strong agricultural focus. It is one of the most important, and underused, routes to equipment finance, because it lends to cooperatives and groups, not just individuals, and prioritises group accountability over collateral.

MSC’s asset-financing and community asset lease products are designed exactly for shared machinery: a cooperative pays part of the cost and repays the rest over a lease whose ownership transfers progressively. This is one of the clearest paths for a group of farmers to put a tractor on the ground.

Route 3: Uganda Development Bank (UDB)

UDB is the national development bank, lending below commercial rates: reportedly around 10–12% per year, with long terms (up to around 15 years) and grace periods of one to three years. It explicitly funds agricultural mechanization, value addition, processing and storage. UDB tends to target larger, SME-scale projects, so smallholders usually access it through a cooperative or aggregator rather than as individuals.

Route 4: Asset financing and supplier credit

Dealers and financiers increasingly offer hire-purchase: pay a deposit (often around 20%), take the machine, and repay over time with the asset as security. New models, including pay-as-you-go and collateral-free schemes from equipment-finance partners, are spreading in Uganda. The key is to read the total cost and the repossession terms carefully before committing.

Route 5: Government programmes

The Parish Development Model (PDM) channels funds through parish-based SACCOs, UGX 100 million per parish per year, lending to enterprise groups of subsistence households at about 1% interest as a revolving fund. Programmes like aBi (Agricultural Business Initiative) and donor-funded activities support the sector indirectly, mostly by lending to or guaranteeing financial institutions that then lend to farmers. These are worth asking your SACCO and district about.

How to qualify, and not over-borrow

Join and build a savings record

Membership and a few months of consistent saving unlock both SACCO loans and the group channels that MSC, UDB and PDM lend through.

Borrow as a group for big assets

A tractor is best financed by a cooperative or group that shares the machine and the repayment, not by one household stretching alone.

Time repayment to the harvest

Match the repayment schedule to when crop income actually arrives. Inflexible monthly schedules are a leading cause of default.

Size the loan to one production cycle

Borrow only what one realistic harvest can repay. With seasonal income and weather risk, over-borrowing is the trap that sinks farmers.

The over-borrowing trapAt 2–3% per month, a loan that outlasts your harvest compounds fast. Combined with a bad season, that is how farmers lose assets. Keep the term inside one production cycle and the size inside one harvest's realistic revenue.

NUTOFA brings the savings, the loans and the machines together in one membership. Explore our savings and loan products, the mechanization hub, or become a member.

- Microfinance Support Centre: conventional finance, asset financing and community asset lease products; lending to SACCOs/cooperatives, 2026; allAfrica reporting on MSC terms, May 2026.

- Uganda Development Bank: agricultural financing terms (indicative ~10–12% p.a., long tenors); Ministry of Finance create.finance.go.ug, 2026.

- Bank of Uganda / Daily Monitor: average commercial lending rates ~18% and agriculture ~21.5% (FY2023/24), 2024.

- Presidential Initiatives / Ministry of Finance - Parish Development Model: UGX 100m per parish, ~1% revolving fund, 2023–2024.

- aBi (Agricultural Business Initiative): lines of credit and loan-guarantee scheme to financial institutions, 2026.

Frequently asked questions

-

The realistic routes are: a savings-backed loan from a SACCO or cooperative; asset financing or a community asset lease through the Microfinance Support Centre; agricultural lending from Uganda Development Bank (usually via a cooperative or larger project); supplier hire-purchase; or pooling resources as a group so the machine is shared. Few smallholders buy a tractor alone: most access one through a cooperative.

-

It varies widely by lender. Commercial banks averaged roughly 18–21% per year, with agriculture at the higher end. SACCOs commonly charge around 2–3% per month. The Microfinance Support Centre lends to cooperatives at roughly 8–9% per year, and Uganda Development Bank around 10–12% per year. Always confirm whether a rate is per month or per year, and flat or reducing balance.

-

Yes. A SACCO lends against your savings and member guarantors rather than a land title, and the Microfinance Support Centre prioritises group accountability over collateral for cooperatives and groups. This is the main reason cooperatives are the practical entry point to equipment finance for smallholders.

-

Asset financing lets you acquire equipment by paying part of the cost upfront (often around 20%) and repaying the rest over time, with the asset itself serving as security. A related option, a community asset lease, lets a cooperative or group acquire shared machinery whose ownership transfers progressively as the lease is paid.