The genius of a SACCO is simple: your savings are both your safety net and your key to credit. But “save and you can borrow three times your savings” raises a lot of practical questions: three times what, exactly? What are the different savings for? Who guarantees the loan? This guide answers them with worked shilling examples, using NUTOFA’s products as the illustration.

- You build four kinds of money: compulsory savings, voluntary savings, shares and welfare.

- Your loan ceiling is a multiple of your savings: NUTOFA uses 3×.

- Loans are guaranteed by fellow members, not a land title.

- Surplus comes back to you as a dividend on your shares, voted at the AGM.

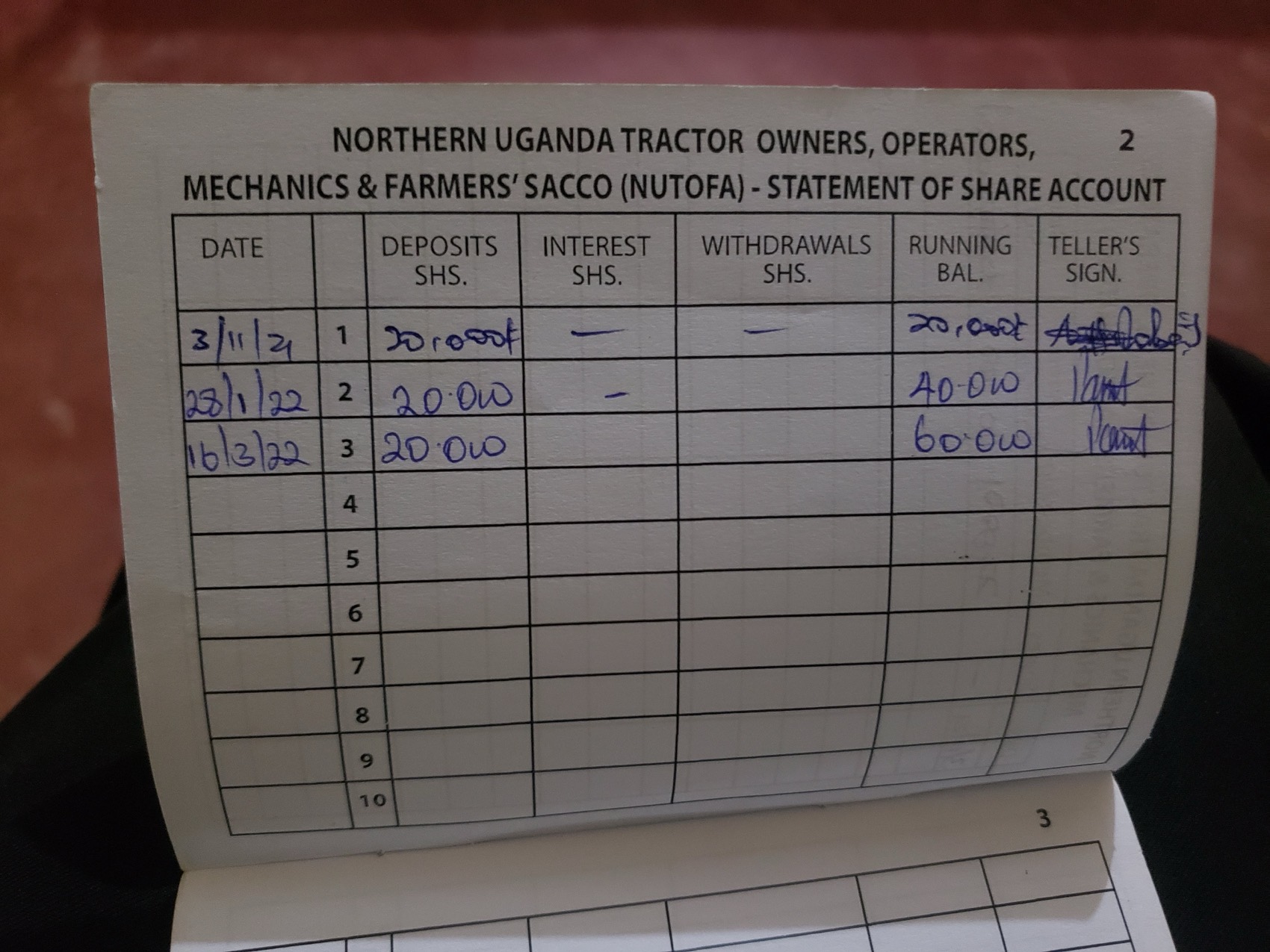

The four kinds of money in your account

When you join, you start building several different balances. They do different jobs, and it pays to understand each.

| Type | What it does | Withdrawable? | Counts toward loan? |

|---|---|---|---|

| Compulsory savings | Fixed regular deposit every member makes | On notice | Yes, builds your ceiling |

| Voluntary savings | Extra you choose to save; earns modest interest | On notice | Supports your standing |

| Shares | Your ownership stake; earns dividends | Transferable on exit | Generally no |

| Welfare fund | Group social protection for emergencies | Per welfare rules | Backs welfare loans |

The key mental model: shares make you an owner (and earn dividends), while savings make you a borrower (and earn you a loan ceiling). You want to build both.

How the loan ceiling actually works

This is the part most people half-understand. SACCOs lend against your savings record, not your land, so your borrowing power grows as you save. NUTOFA uses a three-times-savings ceiling.

Worked exampleSave UGX 20,000 a month for 12 months → UGX 240,000 in standing savings. At a 3× ceiling, you can borrow up to UGX 720,000. Keep saving to UGX 500,000 and your ceiling rises to UGX 1,500,000. The more you save, the more you can borrow.

Two things follow from this. First, consistent saving is the lever: every shilling you save lifts your ceiling. Second, your savings aren’t “locked up doing nothing”; they are simultaneously your buffer, your dividend base, and the collateral that unlocks a loan several times their size.

The main loan products

A good agricultural SACCO offers loans shaped to the farming year, not generic ones. These are NUTOFA’s products as an example:

Mechanization loan

For tractor purchase, implement repair, fuel and operating cash, for owners and mechanics. Term 3–9 months, grace negotiated per season.

Agricultural loan

Smallholder working capital timed to planting and harvest. About 5 months, with a grace period of up to 4 months so repayment lands after you sell.

Emergency loan

A same-day bridge for medical, school-fees or harvest cash needs, short (≤30 days), so you never have to dump your harvest in a distress sale.

Asset financing & welfare loans

Structured supplier financing for tractors and implements; and welfare loans drawn against the welfare fund for member emergencies.

Guarantors: trust instead of title

Because there’s no land title behind most loans, the SACCO relies on member guarantors. To borrow, you typically need one or more guarantors who are members in good standing, whose own savings help cover your loan. This is the social engine of the model: members vouch for each other, which both extends credit to the landless and keeps default low, because your guarantors, your neighbours, are on the hook with you.

Guarantor basicsChoose guarantors who trust you and whom you'd guarantee in return. Honour every guarantee you give: defaulting on someone else's loan you guaranteed can freeze your own savings and borrowing.

Repay with the harvest, not against it

The most farmer-friendly feature of a good SACCO loan is timing repayment to your harvest. Farm income is lumpy: it arrives when you sell. Loan products like the agricultural loan build in a grace period so repayment falls after the harvest, not during the hungry growing months. When you take a loan, match its term and schedule to when your crop money will actually come in. Over-borrowing against a single season is the most common way farmers get into trouble: borrow only what one realistic harvest can repay.

Dividends: the payback of ownership

At the end of the year, after audited accounts, the membership votes at the Annual General Meeting (AGM) on a dividend, your share of the surplus, paid on your shares. It is not fixed interest and not guaranteed; it reflects how the cooperative actually performed. But it means the interest other members pay on loans, and the cooperative’s own business (like hub tractor income), ultimately flows back to the owners, you, rather than to outside shareholders.

Put it together and the cycle is: save consistently → build shares and a loan ceiling → borrow against your savings with guarantors → repay with the harvest → share in the year’s dividend.

Explore NUTOFA’s savings and loan products, how to join, or how to finance farm equipment.

- International Cooperative Alliance: member economic participation, surplus distribution, 1995.

- Representative Ugandan SACCO lending policies: savings-multiple ceilings, guarantor requirements, loan graduation.

- UMRA: SACCO regulation and supervision, 2022.

- NUTOFA SACCO LTD savings and loan product set (3× ceiling; mechanization, agricultural, emergency, asset-financing and welfare loans), 2026.

Frequently asked questions

-

Most SACCOs lend a multiple of your standing savings. NUTOFA uses a three-times rule: if you have UGX 500,000 saved, your loan ceiling is UGX 1,500,000. The exact multiple varies by SACCO, and the loan must be backed by guarantors who are members in good standing.

-

Compulsory savings are a fixed regular amount every member must contribute: they stay yours and count toward your loan ceiling. Voluntary savings are extra amounts you choose to deposit and can withdraw on notice, usually earning modest interest.

-

Your savings and the value of your shares are yours: savings can be withdrawn on notice, and shares are transferable to another member when you exit. The one-off entry/membership fee is non-refundable.

-

A dividend is your share of the SACCO's annual surplus, paid on your shares and declared by members at the AGM. It is not guaranteed: it depends on the year's audited results, and it is a real dividend voted by the membership, not fixed interest.